Combining strong regulation and multiple funding options to deliver EU CCS [Gas in Transition]

Across Europe, in both EU member and non-member states, momentum for carbon capture and storage (CCS) continues at pace, driven by robust policy and financial support mechanisms. As of March 2024, Global CCS Institute data included 178 commercial facilities in either development, construction or operation in the European CCS project pipeline. These facilities have a combined CO2 capture capacity of ~100mn tonnes/year and represent almost a third of the 564 commercial facilities in the pipeline globally. North America however, continued to be the frontrunner for CCS projects and deployment, with some 291 projects in the pipeline, led predominantly by projects in the US.

In both the US and Europe, the number of CCS projects in the pipeline has surged and shown strong year-on year growth for several years now. This has been spurred by crucial government support, offering attractive financial incentives and strong policy frameworks that shore up investor confidence for projects.

In the US, the 2022 Inflation Reduction Act (IRA) created favourable economic incentives for CCS, especially for production of low emissions hydrogen and ammonia, with enhancement of the 45Q tax credit. Institute analysis of the impact of the IRA concludes that this tool could increase CCS deployment in the US by between 200-250mn t/yr of CO2 by 2030. Other US federal money for CCS is also available through the 2021 Bipartisan Infrastructure Law (BIL), and the 2022 CHIPS Act.

In the EU, the goal of reaching net-zero by mid-century has brought carbon management technologies including CCS, carbon capture and utilisation (CCU) and carbon dioxide removal (CDR) firmly into focus. Recently, the European Commission has supported the acceleration of CCS deployment in the region with a wide range of legislative and regulatory developments under key action plans such as the Fit for 55 Package, the Green Deal Industrial Plan and Sustainable Carbon Cycles. In February 2024, the Commission also released its long-awaited EU Industrial Carbon Management Strategy, outlining an ambitious vision to scale up carbon management solutions in the EU.

To complement this raft of EU legislative and regulatory actions, financial support mechanisms have also been enhanced. These include EU funds, individual national subsidy programs and the carbon price set by the EU Emissions Trading Scheme (ETS). As seen with financial incentives offered in the US, these financial support mechanisms have provided a level of confidence in the economic viability of CCS projects in the EU, particularly in the first phase of deployment, and have become the main drivers for CCS in the EU.

In the case of the EU ETS, in addition to incentivising CCS deployment, the scheme also generates revenue used to contribute to the EU’s Innovation Fund. The fund uses ETS revenue to support innovative low-carbon technologies, with a budget potentially reaching €40bn for 2020-2030, depending on EU ETS prices.

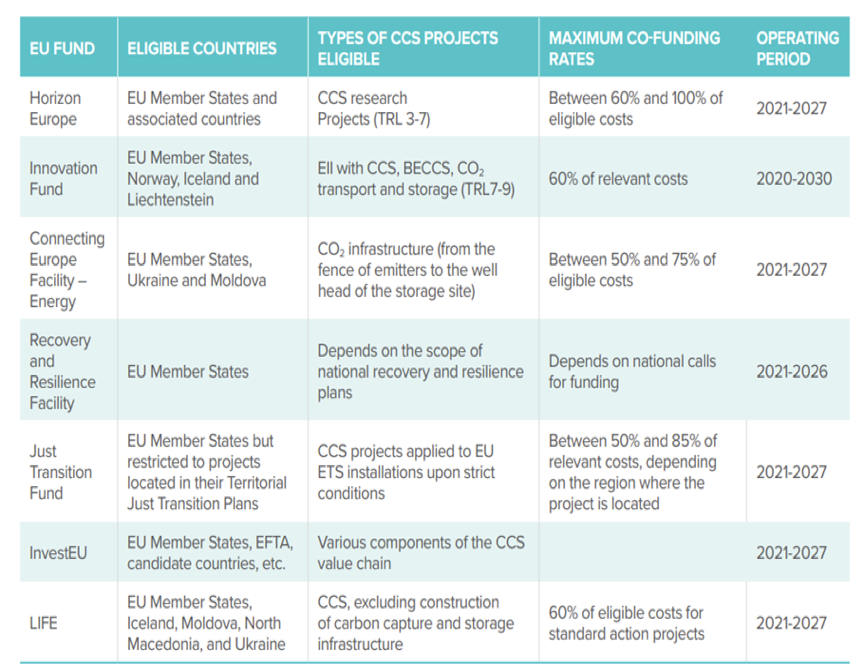

The Innovation Fund is just one of multiple CCS funding options now available in the EU, with financial support for CCS distributed across several funding programs. The other main EU funds include Horizon Europe, Connecting Europe Facility for Energy (CEF-E), the Recovery and Resilience Facility, the Just Transition Fund, the InvestEU Fund, and LIFE.

The choice of EU funding source depends on the nature, scope and geographical location of the CCS project. For example, the CEF-E fund primarily supports Projects of Common Interest (PCIs) and Projects of Mutual Interest (PMIs). These are projects with significant cross-border impacts (such as CO2 infrastructure). On the other hand, the Recovery and Resilience Facility focuses on projects aligned with the reforms and investments defined in the recovery and resilience plan of EU Member States.

To assist in navigating the EU funding options available, the Global CCS Institute has produced a guide to the seven main EU funds - From Proposals To Reality: How EU Funds Can Help Jump-Start CCS Projects. The table below shows a summary from this report, of the main factors to consider when applying to selected EU funds.

Main elements to consider when applying to the selected EU funds

Source: The Global CCS Institute

The EU also continues to progress and allow other tools that will support CCS momentum. For example, carbon contracts for difference have been recognised in the revised Guidelines on State aid for climate, environmental protection and energy (CEEAG). These allow EU member states to implement this state aid instrument nationally. Several countries, including the Netherlands and Denmark, are already using it for CCS, while others, such as Germany and France, have announced plans to do so.

Belgium, Denmark, France, Germany, Iceland, the Netherlands, Norway, Sweden, Switzerland and the UK have all also made progress in bilateral agreements, declarations and/or collaborations on CCS. Additionally, the European Commission is exploring the potential regulation of CO2 transport, which could introduce regulated tariffs for CO2 networks at EU level.

Throughout Europe, favourable government support and conditions for CCS are promoting greater collaboration across industries and borders (regardless of EU status), as the urgency for CCS deployment intensifies globally. CCS is taking an all-Europe approach, with countries like Italy, Greece, Romania, Bulgaria, and the Baltic states making advancements in CCS, in addition to the North Sea countries that were the first movers.

For the world to achieve its shared climate targets an annual CO2 storage rate of approximately 1 Gt/yr by 2030 will be needed, with multiple Gt/yr required by 2050. In providing attractive funding and financial incentives for CCS, coupled with strong regulatory and policy support, the EU is creating an environment where scale-up of CCS projects is possible - keeping our ambitious global climate targets within reach. The results are evident in the continued growth of CCS pipeline projects across the region, providing reason to be optimistic about the future of CCS deployment across the EU and Europe.

The Global CCS Institute is an international think tank whose mission is to accelerate the deployment of carbon capture and storage (CCS), a vital technology to tackle climate change and deliver climate neutrality. For more information, visit www.globalccsinstitute.com