New lease of life for Canada’s LNG projects? [Gas in Transition]

LNG pricing has recovered remarkably from the pandemic and supply-side induced lows of 2020, driven by a global recovery in energy demand and, in particular, Asian thirst for the fuel. China looks certain to emerge as the world’s largest LNG consumer this year, relegating Japan to second place for the first time on an annual basis.

Asian buyers have been willing to pay more than $20/mn Btu for spot cargoes, record levels for this time of the year, as they stock up ahead of the northern hemisphere winter. Available cargoes have been diverted from the Atlantic basin, leaving Europe short and pushing European gas hub prices to high levels.

But at these prices, Asian and European buyers are reverting to higher carbon fuels and interest in expanding LNG import capacity may falter.

Across Europe, coal-fired plant is being ramped up or brought back into service amid low wind levels to ensure there is sufficient operational generation capacity over the winter. For many coal plants, this is likely to be their last hurrah.

Countries such as the UK, France and Italy have policies in place which will phase the fuel out of their generation mixes over the next three to five years, leaving them more reliant on natural gas for both flexible and baseload generation at times of high demand.

In Asia, China’s rising consumption of LNG is being driven by coal-to-gas replacement, even as Beijing seeks to expand its renewable energy capacity. Similarly, Japan and South Korea’s immediate fall back in the face of high LNG prices will be to burn more coal and oil.

The message appears clear: more renewable energy capacity and system flexibility is essential, but LNG capacity also needs to grow to bring prices back to more affordable levels, avoid a short-term recourse to higher carbon fuels and prevent such a reoccurrence over the medium to long term.

Sleeping giant

Asia generated 7,386 TWh of electricity from coal in 2020, 78.4% of the world total and more than five times the amount of renewable energy generation across the continent. Sitting across the Pacific, with shorter vessel journeys than any LNG produced in the Atlantic basin, lies Canada with abundant gas resources.

In its 2021 World LNG report, the International Gas Union cited 227.8mn mt/yr of proposed LNG projects in Canada at the pre-FID stage, of which 179.3mn mt/yr were on the West Coast. The vast majority of those, however, have fallen by the wayside and are unlikely ever to advance to FID.

Canadian LNG projects have struggled to make headway, but 2021 is providing a major market turnaround from the doldrums of 2020, when US LNG production had to be shut in and the prospects for new LNG capacity worldwide appeared bleak.

Canada versus the US

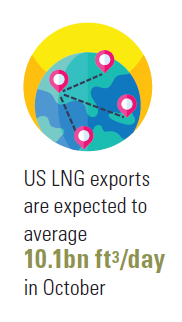

There is no question that US LNG developers have stolen a march on their northern neighbour. US LNG exports in September averaged 9.3bn ft3/day in September and are expected to average 10.1bn ft3/day this month, according to the most recent forecasts from the US Energy Information Administration. In contrast, Canada has only one major LNG plant under construction, LNG Canada, which is expected to see its first cargo leave in 2025.

A second project, Woodfibre LNG, also has momentum. The project landed a second off-take agreement with UK oil major BP in May for 0.75mn mt/yr over 15 years on a free-on-board basis. This takes BP’s commitment to 1.5mn mt/yr from the proposed 2.1mn mt/yr plant. Woodfibre LNG hopes to make a final investment decision soon.

A second project, Woodfibre LNG, also has momentum. The project landed a second off-take agreement with UK oil major BP in May for 0.75mn mt/yr over 15 years on a free-on-board basis. This takes BP’s commitment to 1.5mn mt/yr from the proposed 2.1mn mt/yr plant. Woodfibre LNG hopes to make a final investment decision soon.

The US has been able, literally, to build on past mistakes, using brownfield sites (former LNG import terminals) to reduce investment costs, while also taking advantage of the huge quantities of gas produced alongside the country’s shale oil boom and an existing well-developed gas pipeline network and market.

Canadian LNG projects, in contrast, are much more dependent on greenfield development, including for upstream gas supply and pipeline infrastructure, all of which bring attendant permitting, development and construction challenges.

However, US LNG development also has its weaknesses, the primary one being the failure to develop LNG capacity on the country’s west coast, from where journey times and costs to the dynamic demand markets of Asia are shorter and lower. To get to Asia, US LNG has to pass through the Panama Canal, which adds costs and, despite its expansion, the canal still suffers congestion, resulting in delivery delays and sometimes re-routing.

Notably, one of the few LNG projects to receive a positive final investment decision in recent years was Sempra Energy’s Costa Azul project, a brownfield conversion of a west coast LNG import terminal sited not in the US but in Mexico, with the feed gas coming across the US-Mexican border.

Social license

Canadian LNG thus has two primary hurdles to jump. First it has to compete for investment dollars with projects elsewhere in the world, and to date this is a battle with few victories. Having gas in the ground and good seaborne transport economics is necessary but not sufficient. Costs must be acceptable and permitting possible.

Unlike LNG projects in the US, Middle East, Africa or even Australia, amid a complex federal political system, Canada faces numerous construction and permitting challenges to site greenfield LNG plants and build the long pipelines needed to get gas to coastal export points.

A case in point is the long-standing west coast Kitimat LNG project, which suffered a major blow at the end of 2019, when 50% shareholder and operator Chevron announced that it would divest its interest. In May this year, Australia’s Woodside, which holds a 50% non-operated share, announced it would exit the project. Both companies cited a desire to invest in higher value projects in other countries.

Environmental challenges

The second major hurdle is LNG’s environmental profile. Numerous studies suggest that LNG supply chains to Asia result in carbon emissions reductions as coal and oil use are displaced. However, many environmental organisations contest the findings and oppose what they see as a long-term lock-in for fossil fuel use, owing to the multi-billion dollar investments needed to get LNG supply chains up and running. They argue these funds could be better spent elsewhere on renewable energy and other clean energy transition technologies.

In July, GNL Quebec’s proposed LNG plant at Port Saguenay was rejected by the Quebec government on environmental grounds. The provincial government said the project would not lead to a reduction in GHG emissions and could discourage natural gas users in Asia and Europe from switching to cleaner energy sources. GNL had argued that the plant would be carbon neutral and encourage an overall reduction in GHG emissions as a result of coal-to-gas switching.

Meanwhile, the relatively small FortisBC owned Tilbury LNG plant on the west coast is seeking an expansion of its capacity. The plant has existed as a peak shaving facility since 1971, with about 60 mt/day of liquefaction capacity and 28,000 m3 of storage. A Phase 1A expansion added 46,000 m3 of new storage and 700 mt/day of new liquefaction capacity in 2018, while Phase 1B work contemplates another 2,000 mt/day of liquefaction capacity, expected to come online in the 2024-2025 time frame.

A Phase 2 expansion plan is now before environmental regulators. It would add 142,400 m3 of storage and up to 7,700 mt/day of liquefaction capacity but has encountered opposition both on environmental grounds and because the plant is located near urban areas.

Project evolution

Still, Canada’s LNG developers are responding to the challenge. While market conditions look increasingly positive, they are re-designing their projects with GHG emissions as a baseline concern.

In July, Calgary-based Pieridae Energy announced that its east coast Nova Scotia Goldboro LNG project would not go forward as formerly envisaged. Cost pressures and time constraints relating to Covid-19 were cited as reasons by the company’s CEO Alfred Sorensen.

While on hold for the moment, the company is going back to the drawing board, looking at a floating LNG concept, which it believes could drastically reduce the project’s GHG emissions. This could be coupled with both carbon capture and ‘blue’ power development.

When it returns to the market, Goldboro LNG could look very different from its initial conception, with GHG reductions front and centre of its proposal.

A newly-proposed project, Ksi Lisims LNG, which filed its initial project description at the end of July, provides another example. Rockies LNG, Western LNG and the Nisga’a Nation have proposed a 12mn mt/yr floating LNG plant on Canada’s northwest coast.

The project is targeting net zero carbon emissions from the operation of the plant from the outset. This is to be achieved through the use of renewable electricity to power the plant, a strong monitoring and measurement regime, energy efficiency, the purchase of carbon offsets and potentially carbon capture and storage. The current project timeline is for construction to start in 2024 and for the site to be operational in 2027 or 2028.

And the Haisla Nation, on whose traditional territory the Anglo-Dutch Shell-led LNG Canada project is being built, has advanced its own project, the 3mn mt/yr Cedar LNG proposal, in partnership with Calgary’s Pembina Pipeline, which has all but abandoned its 7mn mt/yr Jordan Cove LNG project in Oregon. It too would be powered by BC’s hydroelectric resources.

Asia’s addiction to coal is extreme, but understandable, as just with many more developed regions, coal was the cheapest and most readily available fuel to power economic growth. But with the climate emergency ever more urgent, large-scale lower carbon solutions are required within the next decade, leaving open the opportunity for Canadian LNG developers to come forward with best-in-class project proposals able to earn a social license to progress.

Project profile: Woodfibre LNG

Project profile: Woodfibre LNG

Woodfibre LNG has made good progress this year, landing a second offtake agreement, which is essential for securing investment finance at a reasonable cost.

The project will tap into Canada’s current gas supplies rather than develop greenfield resources. It will thus be the first export project to drain some of Canada’s gas surplus, which has steadily backed up as the US has developed its shale gas resources.

Pacific Oil & Gas (PO&G), a privately-owned Indonesian company, is developing the project. PO&G is owned by Singapore’s Royal Golden Eagle group of companies.

In June 2019, PO&G completed the acquisition of Calgary producer Pacific Canbriam Energy, gaining an already-producing asset base in the prolific Montney shale gas area of British Columbia and Alberta. UK major BP became the foundation buyer with an offtake agreement for 0.75mn mt/yr, a deal which it has doubled in a separate agreement this year.

The project, which has a license to export for 40 years, has its LNG facility permit from provincial regulator the BC Oil and Gas Commission, alongside three major environmental assessment approvals, including a first-of-its-kind environmental approval from the Squamish First Nation, on whose traditional territory the C$1.8bn project will be built.

Woodfibre LNG will be built on an industrially-zoned site which formerly housed a paper mill that closed in 2006. Woodfibre officially became the owner of the site in 2015, following an extensive clean-up of contaminated sediment, wood chips, equipment and creosote panels left by the paper mill operations. Remediation efforts have continued under Woodfibre’s stewardship.

The project, located in the traditional Squamish village of Swiyat on unceded Squamish Nation lands, is expected to create up to 650 construction jobs and about 100 full-time operational jobs.

The site has a deep-water port and is connected to Canadian utility BC Hydro, which will allow the facility to be powered largely by renewable electricity, reducing its carbon footprint. Using BC Hydro power will, according to Woodfibre LNG, make its facility one of the cleanest LNG plants in the world. The processing facility will also be cooled by air rather than seawater as part of an environmental agreement with the Squamish First Nation.

Feedstock for the plant will be supplied by the Eagle Mountain-Woodfibre gas pipeline project, a 47-km, 24-inch extension of the existing FortisBC gas pipeline running between Coquitlam and Woodfibre near Squamish. This pipeline was built in 1990 and serves Squamish, the Sunshine Coast and Vancouver Island. PO&G has also been in talks with BP Canada regarding transportation and balancing services for gas supplies to the planned LNG export facility.

Project profile: LNG Canada

Project profile: LNG Canada

It took a powerful combination of forces to get Canada’s flagship LNG project, LNG Canada, up and running. The companies behind the venture on the production side are Anglo-Dutch major Shell (40%) and Malaysia’s Petronas (25%), two companies with a long history of cooperation in the LNG sector.

It also has major involvement from Asian LNG buyers, representing the world’s three largest LNG markets; Japan’s Mitsubishi (15%), China’s PetroChina (15%) and South Korea’s Kogas (5%), the world’s single largest LNG importing company. Mitsubishi has secured two off-take agreements with Japanese companies Tokyo Gas and Toho Gas.

The project is a major investment for British Columbia, coming with a price tag of $40bn, of which $18bn will be spent on the two-train, 14mn mt/yr first phase now under construction. A second phase would double capacity to 28mn mt/yr, with a final investment decision expected on that before the first phase is completed.

The plant will be powered by a combination of gas-fired turbines and electricity generated by BC Hydro, with the use of renewable electricity reducing the plant’s carbon footprint.

The plant is located at Kitimat at the head of the Douglas Channel, about 650 km northwest of Vancouver.

Construction of the first two trains is expected to take about five years. Storage capacity at full build out will be 450,000 m3. The storage tanks will hold the LNG until it is piped via two cryogenic transfer lines to the wharf and LNG carriers. An existing wharf will be redesigned to berth two LNG carriers at a time each with capacity between 140,000-265,000 m3. The carriers will be brought into the wharf at low speeds by up to three tugboats.

A rail yard will also be constructed and connected to the Canadian rail system. This will be used to load condensate, a petroleum liquid by-product of the liquefaction process. The plant will draw water from the Kitimat River, which will used in a closed-loop system and treated at a water treatment facility before any residual water is returned.

The under construction Coastal GasLink pipeline runs 670 km from the Dawson Creek/Montney area to Kitimat. The pipeline is being built, owned and operated by TransCanada. The pipeline is expected to cost $6.6bn with initial capacity of 1.7bn ft3/d (48mn m3/d). Shell, Petronas, Mitsubishi and Cnooc are all expected to develop existing upstream resources to feed the LNG plant.